updated 12/9/21

New leadership at the US Department of Education has begun taking the concerns of public service workers seriously. Earlier this year, after pressure from the AAUP and our allies in the labor and consumer protection movements, the department unveiled significant reforms to the Public Service Loan Forgiveness (PSLF) program to make sure it delivers on its promise of relief.

Since PSLF was created in 2007, borrowers have encountered problem after problem in achieving debt cancellation. Many borrowers with “guaranteed” or Family Federal Education Loans (FFEL) faced issues with getting payments properly counted, or were unaware of the need to transfer their Direct Loans to be managed by a certain servicer in order to have their PSLF paperwork processed. Mismanagement by loan servicers was exacerbated by clunky federal regulations tied to annual employer certification and the final application process. This all led to nearly 98 percent of applications being denied forgiveness.

But, after nearly 50,000 public comments from borrowers and an internal audit of borrowers eligible for PSLF, the department has taken a series of steps to resolve long standing issues with the troubled program.

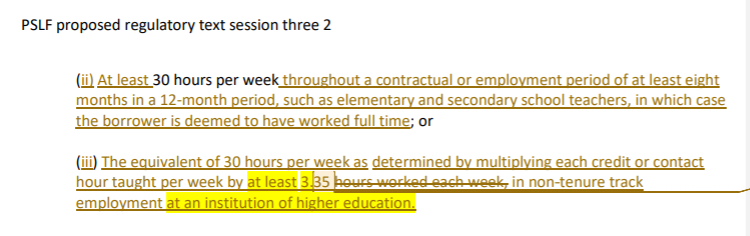

First, the department announced its intent to revise the existing regulations to improve servicing for those with older types of loans, to improve income-driven repayment plans through which borrowers pursue PSLF, and to expand eligibility to new kinds of employers and employees. This process happens via a negotiated rulemaking committee, where a committee of stakeholders (such as borrowers, colleges and universities, lenders, and consumer advocates) edit draft regulations proposed by student lending experts at the Department of Education. Crucially for AAUP members, the department has proposed creating a credit-hour-to-work-hour conversion so that more contingent faculty could hit the 30-hour eligibility threshold of “full-time employment” required for PSLF. We’re excited to see the recognition of the high workload and low pay that contingent faculty face, but as the AAUP’s David Kociemba noted in his testimony, the formula needed to be more generous.

In its final week of rulemaking meetings, the committee did not reach consensus on reforms to PSLF, but the department did improve its proposed credit-hour workaround to recognize each credit hour a faculty member teaches as 3.35 work hours; this means that, if the proposal makes it into the final rule, a so-called “part time” faculty member teaching at least 9 credit hours would become eligible for PSLF. This new regulation could have an emormous impact if implemented early in the new year: faculty currently working full time could get retroactive recognition of the years of payments they made while working part time. We’ll continue working behind the scenes to ensure that more faculty are able to access PSLF, and will alert members when the department issues a final rule for public comment in the spring. We hope that after widespread support from negotiators, the credit-hour rule makes the cut.

Second, the department settled a lawsuit filed by the American Federation of Teachers (AFT) and the National Student Legal Defense Network, implementing further reforms to the management of PSLF. In addition to creating a formal appeals process for denied applications for PSLF, the department promised to review applications denied by the previous presidential administration and to improve communication to those denied, so that they would be given directions on how to successfully file for debt cancellation. The department also agreed to improve the application process by allowing mass digital annual recertification by employers, automating the application process for federal employees, and more. These moves signal the department’s intent to further streamline the process in the future.

Finally and most significantly, the department announced a special waiver period through October 2022 to resolve widespread servicer error in counting payments, particularly for consolidated loans. Some borrowers with Direct Loans will receive personalized emails updating them on how many previously uncounted payments will be added to their account; waves of emails notifying borrowers began in October 2021 and are ongoing as the department continues its audit of the student loan portfolio. Beyond the borrowers receiving automated messages, any federal student loan borrower otherwise eligible for PSLF but in the wrong kind of repayment plan can benefit from this special waiver period. If a borrower has made ten years of payments in the wrong plan, they may file an application for forgiveness; if a borrower is under a decade of service, they may transfer their loan to the correct repayment plan and get their payments retroactively counted towards forgiveness.

As thrilled as we are to see regulations change in response to borrower needs, we understand that these changes add even greater complexity to an already complicated process. The AAUP is here to help make sense of these changes and help our members get on track for the debt cancellation that you are entitled to.

To help AAUP members, we’re providing some new resources to help navigate the special waiver period, with more to come:

-

Self-guided resources

The Student Borrower Protection Center, a nonprofit founded by former regulators to advocate for student lending reform, has created a series of videos to walk borrowers through the application process for PSLF. Their short video “Overview of Recent Changes to PSLF” is a great place to start. The PSLF tip page includes answers to frequently asked questions, step-by-step videos on consolidating your loans, and state-based resources for filing a complaint.

-

Group information sessions

As part of our joint organizing partnership with the AFT, our members will soon have access to student debt clinics run by AFT staff and elected leaders who are experts in navigating the complex world of student lending rules. This presentation has been updated to include the latest changes to PSLF, on top of the usual review of lower-cost income-driven repayment plans and refinancing options. Attendees are welcome to ask questions during the live information session or to follow up privately. You can sign up for the waitlist to be notified when registration opens for our student debt clinics here.